Key Takeaways

- Most buyers close within 30 to 60 days after their offer is accepted.

- From starting your search to getting the keys, the full home buying process typically takes 2 to 6 months.

- Since there is no mortgage underwriting involved, cash purchases can sometimes close in 7 to 14 days.

- New construction and short sales usually take longer than a traditional resale purchase.

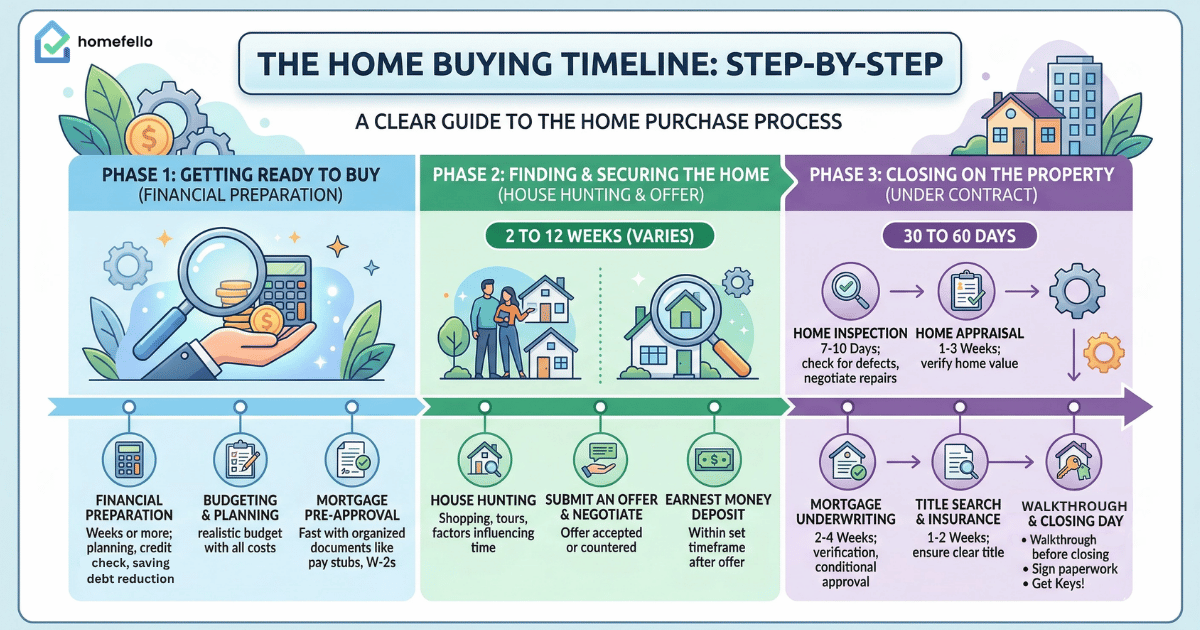

The Home Buying Timeline, Step by Step

The home buying process is usually easiest to understand in three main phases:

- Getting ready to buy

- Finding and securing the home

- Closing on the property

Phase 1: Financial Preparation

Depending on your financial planning up to the point in which you’re ready to begin searching, the preparation phase can take weeks or longer. Buyers who have saved their down payment and other associated costs needed to buy a home may only need to gather documents and get pre-approved and can move much faster. Others who are newer to the process will likely need time to save their down payment, possibly reduce debt and ensure their credit score is in a healthy range.

Budgeting, Planning and Pre-approval

Before a buyer can do anything, it’s imperative that they understand the full picture of their financial house. This includes knowing their credit score and checking their credit report for errors, paying down high-interest debt, avoiding new credit inquiries and building a dedicated savings buffer.

Once a healthy financial baseline is established, the next most important step is establishing a realistic budget. This number needs to include not just the list price, but also the down payment, closing costs, homeowners insurance, property taxes and ongoing maintenance. Having a combined monthly figure in mind, instead of solely targeting a listing price range, typically helps speed up the process. Many buyers use a mortgage calculator to estimate monthly payments before touring homes.

-Finally, buyers will typically pursue mortgage pre-approval, which is different from pre-qualification. A pre-approval generally involves verifying income, assets, employment and credit so you have a stronger sense of what you can afford. It also signals to sellers that you are a serious, prepared buyer.

What you may need for pre-approval:

- Recent pay stubs or proof of income

- W-2s or tax returns (especially if self-employed)

- Bank statements and proof of assets

- Authorization for a credit check

- Information on current debts (student loans, car loans, credit cards, etc.)

If you have these items ready and can respond quickly to lender requests, pre-approval can move fast. Keeping documents organized in a single folder and avoiding new credit activity during this period can also prevent unnecessary follow-up questions. If you are self-employed, have variable income, or need time to document assets, it can take longer.

Phase 2: House Hunting and Making an Offer (2 to 12 Weeks)

This is the phase where timelines tend to vary the most. Some buyers find the right home in a weekend. Others tour homes for months, especially in hot markets where inventory is lower.

Several factors influence how long shopping takes:

- Inventory and competition: Fewer listings usually means more buyers chasing the same homes.

- Budget flexibility: The wider your search criteria, the easier it can be to find a good match.

- Timing and seasonality: In many markets, spring and summer are more active, leading to increased competition.

- Your decision-making process: If you and a partner or family need to align on priorities, it can add time.

Once you find a home you want, you will submit an offer to the seller. Your offer may be accepted, rejected or countered with negotiations around price, closing date, included appliances, repairs and contingencies.

In some cases, an offer is accepted the same day. On the other hand, buyers and sellers may go back and forth for several days, especially if the seller receives multiple offers or has a specific timeline.

After your offer is formally accepted and the contract is signed, you will typically provide an earnest money deposit within a set timeframe outlined in the agreement, usually within a few days. The deposit is held in escrow and later applied to your purchase, though the exact timing and terms depend on your contract and contingencies.

Phase 3: Under Contract (30 to 60 Days)

Once your offer is accepted you are under contract. From here, the closing timeline becomes more predictable. This is also the phase where most delays occur, since inspections, appraisals, underwriting and title work all have to align before funds can be released. While the process generally follows a structured sequence, small documentation issues, scheduling conflicts or repair negotiations can extend the timeline.

The remaining timeline generally follows a predictable sequence: inspections, appraisal, underwriting, title work and final signing.

Home Inspection (7 to 10 Days)

While not technically required (especially in competitive markets), many contracts include an inspection contingency with a defined time window, often around a week. It’s generally a good idea and gives you peace of mind as a new homeowner. During that window, the buyers will schedule a professional inspection and review the results.

A standard inspection looks for major defects and safety issues, such as problems with the roof, foundation, electrical systems, plumbing, HVAC and signs of water damage. The inspector will usually provide a report with photos and notes.

After the inspection, you typically have a few options:

- Proceed as-is

- Ask the seller to make repairs

- Request a credit or price reduction to cover repairs

- Walk away, if your contract allows it

Inspection negotiations are one of the most common places timelines become extended. Scheduling the inspection as soon as the contract is signed can help preserve your full contingency window. If the report reveals significant issues, you may need additional specialty inspections, contractor estimates or time for the seller to complete agreed upon repairs.

Home Appraisal (1 to 3 Weeks)

If you plan on financing the home with a mortgage, your lender will order an appraisal to confirm the home’s value. The appraiser evaluates comparable sales and the home’s condition to estimate market value.

Appraisals can take longer when:

- The market is busy and appraisers have limited availability

- Comparable sales are hard to find

- The property is unique or in a rural area

If the appraisal comes in at or above the purchase price, the process usually continues.

If the appraisal comes in low, you may need to renegotiate with the seller, bring additional cash to closing, dispute the appraisal or change loan terms. Low appraisals can add time and, in some cases, cause deals to fall through.

Mortgage Underwriting (2 to 4 Weeks)

Underwriting is the lender’s process of verifying that you meet their loan requirements. This is when they will do a comprehensive check of your documents, confirm income and employment, reviews your assets and ensure that the property meets the loan’s criteria.

Many buyers receive a conditional approval first. That means the lender is willing to approve the loan as long as you satisfy certain “conditions,” like providing updated bank statements, clarifying a deposit or submitting additional documentation.

Underwriting delays often happen because:

- Documents are missing or outdated

- Employment verification takes time

- Large deposits require additional explanation

- The lender is handling high volume

The best way to keep underwriting moving is to respond quickly to document requests and avoid major financial changes during this period. For example, buying a car, opening a new credit card or moving large sums of money between accounts can trigger additional lender review and slow down your approval, so it is recommended that you avoid those or similar actions.

Title Search and Insurance (1 to 2 Weeks)

The title company (or attorney, depending on your state) will conduct a title search to confirm the seller has legal ownership and that there are no unresolved claims or liens on the property.

Title work can take longer if the home has unresolved liens, boundary disputes, missing paperwork or ownership issues that require legal cleanup.

During this time, you will also arrange homeowners insurance. Your lender typically requires proof of insurance before closing, so requesting quotes early, especially for older homes or properties in higher-risk areas, can help prevent last-minute delays.

Final Walkthrough (24 to 48 Hours Before Closing)

The final walkthrough is your chance to confirm that the home’s condition is consistent with the contract. Buyers often check that agreed-upon repairs were completed, that the home is in the expected condition, and that appliances and major systems appear to be functioning.

Closing Day

On closing day, you will sign the final paperwork and pay the funds needed to complete the purchase. Depending on your location and lender, closing may happen in person, remotely or through a hybrid process.

After the transaction is funded and recorded, you receive the keys.

FAQs About the Home Buying Timeline

Yes, it is possible, but it depends on the market and your financing. Closing within 30 days is more likely when you are fully pre-approved, your lender can move quickly, the appraisal is scheduled promptly, and there are minimal inspection issues. Cash purchases may close even faster, though title work and scheduling still matter.

Some cash transactions can close in as little as one to two weeks. With a mortgage, the fastest timelines typically require an experienced lender, rapid document turnaround, and no appraisal or inspection complications.

Often, yes. Cash offers can move faster because there is no lender underwriting the loan. That said, many cash buyers still choose to get an inspection and must complete title work, so “cash” does not always mean instant.

Not always. FHA and VA loans often close on a similar schedule as conventional loans. However, appraisal requirements and lender processes can add time in some situations, especially if repairs are required to meet program guidelines.

Underwriting involves verifying income, assets, employment, debts, and property eligibility. Even small details, like a large deposit or a recent credit inquiry, may require documentation. Lender volume and how quickly buyers respond to conditions also play a role.

Yes. A seller can request a longer closing date, need extra time to move, or run into issues on their side of a linked transaction. In some cases, delays also happen if required repairs are not completed on time.

If closing is delayed, the buyer and seller may extend the contract closing date. Depending on your contract and lender, you may need to adjust logistics like movers, rate locks, and utility start dates. In rare cases, unresolved issues can cause a deal to fall apart.