Buying a home can feel overwhelming, especially if it’s your first time. There are a lot of moving pieces, unfamiliar terms, and important financial decisions along the way. The good news is that the home buying process follows a fairly predictable path. Once you understand each step, it becomes much easier to plan, prepare, and move forward with confidence.

This step-by-step guide walks through the full home buying process, from early preparation to closing day, with context that’s especially helpful for buyers navigating the Michigan housing market.

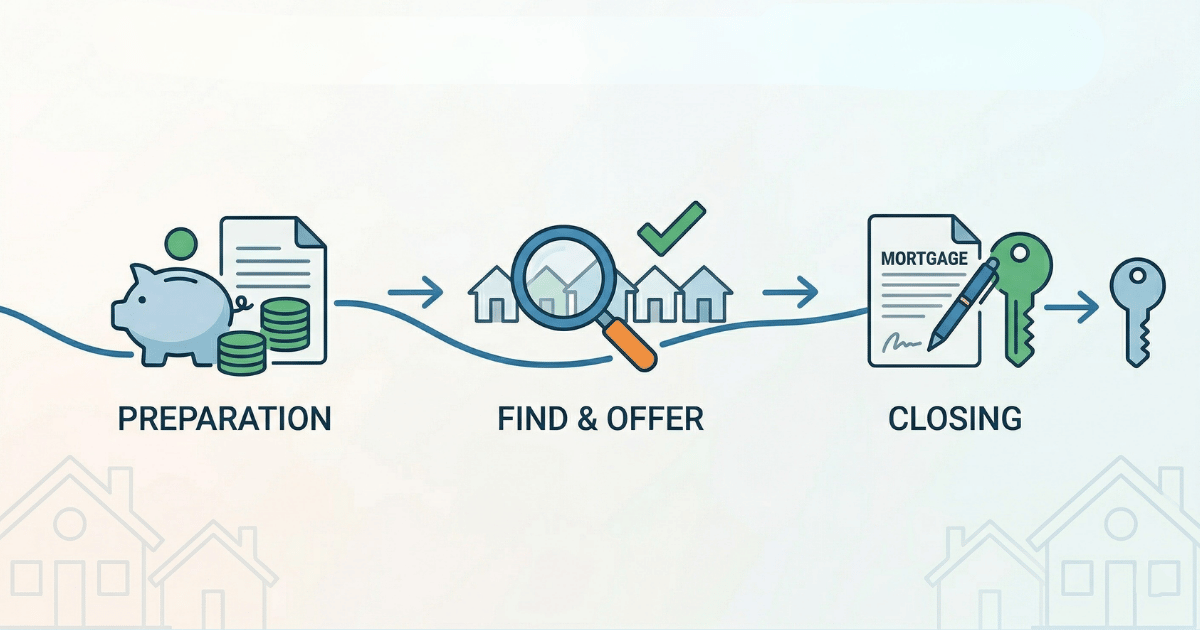

The Home Buying Process at a Glance

For buyers who want a quick overview, here’s how the home buying process typically unfolds:

Each step builds on the last, and understanding the full process upfront can empower buyers to move forward with more confidence.

Step 1: Decide If You’re Ready to Buy a Home

Before you start browsing listings, it’s important to determine whether buying a home makes sense for your financial situation and lifestyle.

Some questions to consider include:

- Are you planning to stay in the area for at least a few years?

- Do you have stable income and manageable debt?

- Are you prepared for upfront costs like a down payment and closing costs?

Many buyers start by using a home affordability calculator to estimate how much house they can reasonably afford based on income, debts, and expenses. This helps set realistic expectations before you fall in love with a home that may be outside your budget.

Beyond the numbers, readiness is also about lifestyle fit. Buying a home means taking on maintenance, property taxes, insurance, and longer-term commitment to a location. For Michigan buyers, that may also include seasonal maintenance, older housing stock, or longer commutes depending on the area you choose.

Step 2: Check Your Credit and Finances

Once you’ve decided you’re ready to buy, the next step is turning that readiness into financial preparation. This is where buyers move beyond broad affordability and start understanding how lenders will actually view their application.

At this stage, buyers should begin planning specifically for their down payment and upfront costs. Beyond knowing what you can afford monthly, understanding how much cash you’ll need on hand helps prevent delays later in the process. Down payment requirements vary by loan type, but buyers should also account for earnest money, closing costs, and reserves required by lenders.

Your credit score, debt-to-income ratio, and savings all work together to shape what loan options are available to you and what interest rate you may qualify for. This is the point in the process where lenders begin translating your financial picture into real borrowing power.

Most buyers use this time to review their credit reports for errors, work to pay down high-interest debt where possible, and organize savings for both a down payment and closing costs. Lenders look closely at patterns, not just snapshots. Consistent on-time payments, stable income, and manageable debt levels matter just as much as your credit score itself.

Getting your finances organized early can make it easier to act quickly once the right home comes along.

Step 3: Choose the Right Mortgage

Before applying for pre-approval, many buyers take time to understand which mortgage option best fits their financial situation. Factors like down payment size, credit score, monthly budget, and long-term plans all influence whether a conventional, FHA, or VA loan makes sense.

At a high level, the most common mortgage options include:

- Conventional loan: Not government-backed, often offers lower interest rates for borrowers with strong credit. Private mortgage insurance (PMI) is typically required if the down payment is less than 20 percent, but it can usually be removed once enough equity is built, reducing long-term costs.

- FHA loan: Government-backed, often has slightly higher interest rates but more flexible credit requirements and lower minimum down payments.

- VA loan: Available to eligible US Military service members and veterans, often features competitive interest rates, no down payment, and no private mortgage insurance.

Choosing the right mortgage upfront can affect not only your interest rate, but also how much cash you’ll need at closing and how flexible your loan terms will be over time.

For a deeper comparison of common loan options, reviewing the differences between conventional and FHA loans can help clarify eligibility requirements and tradeoffs.

Step 4: Get Pre-Approved for a Mortgage

Typical timeline: 1-3 days once documents are submitted

Once you’ve identified the right loan type, mortgage pre-approval is one of the most important steps in the home buying process. It shows sellers that you’re a serious buyer and gives you a clear price range to shop within.

It’s important to understand what pre-approval is and what it isn’t. Pre-approval is not a final loan guarantee, but rather a lender’s conditional approval based on your current financial picture. Your final loan terms can still change if your income, credit, or debt levels change before closing. For many buyers, pre-approval provides clarity and confidence rather than certainty.

During pre-approval, a lender reviews your income, credit, debts, and assets to determine how much you can borrow and an estimated interest rate. This step also helps prevent wasted time touring homes that are out of reach and can make your offers more competitive in fast-moving Michigan markets.

Once you’re pre-approved, maintaining financial stability becomes especially important. Lenders may recheck your credit and income before final approval, so buyers are generally advised to avoid opening new credit accounts, making large unexplained deposits, or changing jobs during this period. Keeping your finances steady helps ensure your pre-approval remains valid through closing.

You can use a mortgage calculator to explore how different loan amounts, rates, and terms affect your monthly payment before or during this step.

Get Pre-Approved Today

We partner with top local mortgage lenders.

Step 5: Start Searching for Homes

Typical timeline: A few weeks to several months, depending on inventory and competition

Once you’re pre-approved, you can begin actively searching for homes within your budget and preferred locations.

Most buyers focus on price range, neighborhood and commute, school districts or nearby amenities, and the type and size of home that fits their needs.

As you tour homes, patterns tend to emerge quickly. Buyers often realize they need to compromise on certain features to prioritize location or affordability. Keeping a clear list of must-haves versus nice-to-haves helps you make confident decisions when the right home appears.

Find Your Dream Home

Browse listings throughout Michigan with easy filters and expert insights to help you narrow in on what’s important.

Step 6: Choose a Real Estate Agent

While it’s possible to buy a home without an agent, many buyers choose to work with a licensed real estate professional who understands the local market.

A knowledgeable Michigan real estate agent can help you identify competitive neighborhoods, advise on pricing and offer strategy, navigate negotiations and paperwork, and coordinate inspections and closing timelines.

Beyond logistics, an experienced agent provides local context. They can explain why homes are priced the way they are, flag potential red flags during showings, and help you move quickly when conditions require it.

Just as important is recognizing when an agent may not be the right fit. Common red flags can include:

Poor communication

Pressure to make decisions you’re uncomfortable with

Limited knowledge of the local market

Lack of transparency around fees and representation

An agent should be willing to answer questions clearly and respect your priorities, not rush you through major decisions.

Choosing the right agent early can make the rest of the process much smoother.

Talk to an Expert Real Estate Agent

We know the real estate landscape in Michigan and are prepared to help you get your dream home, your way.

Step 7: Make an Offer on a Home

When you find a home you want to buy, the next step is submitting an offer on the house. Your offer outlines the price you’re willing to pay and the terms of the purchase.

An offer typically includes:

- Purchase price

- Earnest money deposit

- Requested contingencies

- Proposed closing timeline

Once your offer is submitted, negotiations often follow. This can include back-and-forth on price, closing timelines, repairs, or seller credits depending on market conditions and inspection results.

Offer strategy matters just as much as price. In some cases, flexible timelines, stronger earnest money, or fewer contingencies can make an offer more appealing without increasing the purchase price. Understanding these levers helps buyers compete more effectively.

Step 8: Schedule a Home Inspection and Negotiate Repairs

Typical timeline: 7–10 days after offer acceptance

After your offer is accepted, you’ll usually schedule a home inspection, which is typically paid for by the buyer. Inspection costs vary by home size and location, but many buyers can expect to pay a few hundred dollars out of pocket. A licensed inspector examines the home’s structure, systems, and major components to identify potential issues.

The inspection helps you understand the home’s condition, decide whether to move forward, and negotiate repairs or credits if needed. Inspection fees are generally paid regardless of whether the sale ultimately moves forward, making this an important cost to plan for early.

Inspections are not about finding a perfect home. They are about identifying major issues that could affect safety, livability, or long-term costs. The results often guide important decisions about whether to renegotiate or proceed as planned.

Findings from this process can be especially important in older Michigan homes, where systems and materials may vary widely by neighborhood and age.

Step 9: Complete the Appraisal, Underwriting, and Final Loan Approval

Typical timeline: 2–4 weeks

After inspections and any negotiations are resolved, your lender will order a home appraisal to confirm that the property’s value supports the loan amount. This stage ends with formal loan approval, clearing the way to close. At the same time, your loan goes through underwriting, where the lender verifies all financial information.

During this phase, you may be asked to provide updated documents or clarifications as the lender finalizes your loan. Common requests can include recent pay stubs, updated bank statements, explanations for large or unusual deposits, verification of employment, or documentation for debts or assets that were not previously reviewed. Buyers are also advised to avoid major financial changes during this time.

Underwriting can feel repetitive, but it’s a normal part of the process. Responding quickly to lender requests helps prevent delays and keeps your closing date on track.

Step 10: Secure Homeowners Insurance and Review Closing Costs

Before closing, buyers are generally required to secure homeowners insurance, which protects both you and your lender in the event of damage or loss. In some situations, such as certain cash purchases or specific lender arrangements, this requirement may vary. Proof of insurance is typically required before your loan can be finalized.

You’ll also receive a closing disclosure outlining your final loan terms and all associated costs. These may include lender fees, title fees, taxes, and prepaid expenses. In some cases, buyers may be able to negotiate certain closing costs with the seller as part of the purchase agreement, depending on market conditions and the terms of the offer.

Using a closing costs calculator can help you understand what fees to expect and how they impact your total cash needed at closing.

Step 11: Final Walkthrough and Closing Day

Typical timeline: Final walkthrough occurs 24–48 hours before closing

Shortly before closing, you’ll complete a final walkthrough of the home to confirm it’s in the agreed-upon condition.

On closing day, you’ll sign final loan and purchase documents, pay closing costs and remaining funds, and receive the keys to your new home.

While the paperwork can feel overwhelming, most of the heavy lifting has already been done. Once documents are signed and recorded, ownership officially transfers and the home is yours.

Frequently Asked Questions About the Home Buying Process

From start to finish, the home buying process typically takes between 30 and 60 days once an offer is accepted. The timeline can vary depending on market conditions, financing, and how quickly inspections and underwriting are completed.

While it’s possible to buy a home without an agent, many buyers choose to work with one for guidance, negotiation support, and help navigating paperwork. This can be especially helpful in competitive Michigan markets.

If a seller rejects your offer, you can choose to submit a revised offer, continue negotiating, or move on to another property. Rejection is common, especially in fast-moving markets, and doesn’t mean you won’t find the right home.

Most buyers begin seriously touring homes after receiving mortgage pre-approval. This ensures you’re shopping within a realistic budget and can act quickly when you find the right property. However, browsing home listings as soon as possible will help you get a better picture of what it is you’re looking for in a home.

In most cases, the home inspection happens first, followed by the appraisal. The inspection helps you decide whether to move forward with the purchase, while the appraisal confirms the home’s value for your lender.

Upfront costs usually include an earnest money deposit, your down payment, and closing costs. The exact amount varies based on loan type, purchase price, and location, but planning ahead helps avoid last-minute stress.

What Happens After You Buy a Home?

After closing, responsibilities like homeowners insurance, property taxes, and ongoing maintenance become part of homeownership. Understanding these ongoing costs helps you stay financially prepared long after move-in day.